- PrivateEquityGuy

- Posts

- 20 acquisitions (with the best incentive system possible?)

20 acquisitions (with the best incentive system possible?)

Hint: Rely on specialized know-how that is hard to copy

PrivateEquityGuy

March 27, 2026

Buyers and Builders,

May I ask a quick favor?

If you want me to keep bringing you more world-class business buyers, operators, and investors… and hopefully even more in-person conversations, please take a second to support the show.

Go to your favorite podcast app, follow or subscribe to Buyers & Builders, and leave an honest review, or just rate the show.

Buyers & Builders follower count so far

It makes a huge difference. It helps more people discover the podcast, helps us book even better guests, and allows you to keep learning so you can become (even) better capital allocator as you are today!

Thank you for all the support.

(To show my commitment, I’m traveling to NYC this coming weekend—a schedule fully booked with meetings and a conference, with one goal in mind: to learn and provide as much value as possible to the lower middle market as possible.)

Now, don’t forget to subscribe to and follow the pod.

- - - -

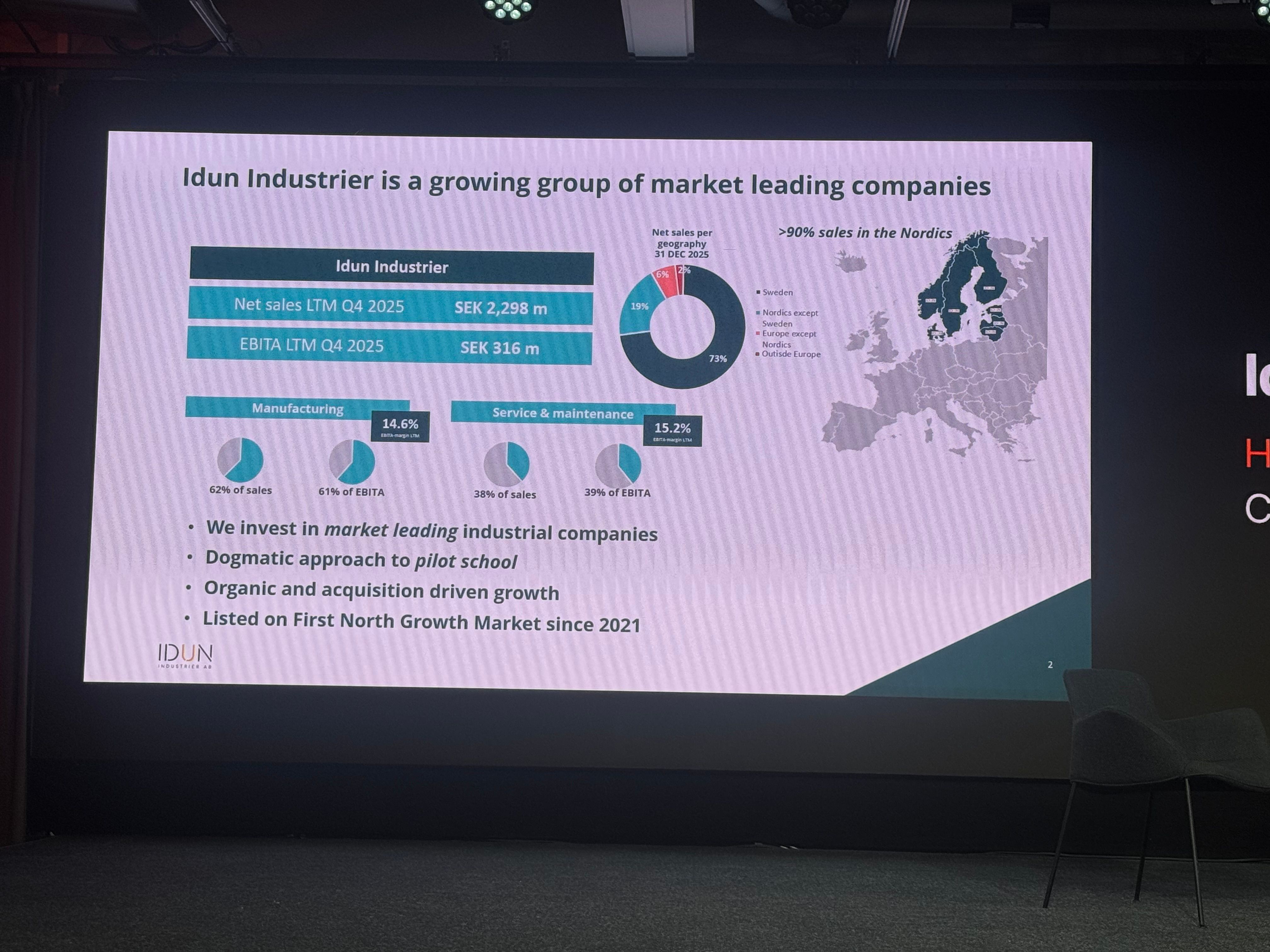

At the recent serial acquirers conference in Stockholm, one of the presentations that has stayed with me came from Henrik Mella, CEO of IDUN Industrier.

I think it’s because of the small niche quality businesses they’ve built…

All of their subsidiaries hold 50%+ market share in their specific niche.

Have you seen a portfolio like this? Me neither.

IDUN has 20 group companies, does about $245-250 million of revenue and about $34 million of EBITDA.

Recurring characteristics of the underlying companies: a strong focus with high market share within one or a few niches and market positions often reflect offerings that are difficult for competitors to replicate.

When people hear “serial acquirer,” they often focus on the deal count, leverage, financing and valuation.

Those things matter.

But they are second-order concerns.

What I find especially attractive is that IDUN does not seem to think like a financial buyer simply assembling a basket of lower-middle-market assets. It appears to think of itself as a long-term owner of very specific kinds of businesses: companies with high market share, defensible positions, and real relevance inside niches that outsiders mostly ignore.

Ownership philosophy and aligned incentives.

Henrik Mella spoke about what he called IDUN’s “pilot school” approach…

The board and management of the parent company are shareholders, and in 100% of the subsidiaries there is co-ownership inside the management teams. Across the group, there are now more than 100 owners, including managing directors and key employees.

A lot of acquirers say they value decentralization. Far fewer build incentive systems that genuinely support it.

Real decentralization is about preserving the ownership mentality at the operating level.

If you want local responsibility, it helps if the local team actually has something real to own, and IDUN seems to understand that.

The intellectual heart of the model is not just “quality.”

It is a market position inside narrow niches.

The word “quality” is thrown around so much it often becomes meaningless. A company can be decent without being special. It can be profitable without being protected.

But when a business holds a dominant share in a small, technically specific market, you often get very different economics.

Better pricing power.

More embedded customer relationships.

Lower competitive intensity.

Specialized know-how that is hard to copy.

And often a market that is too small or too boring for large pools of capital to care about.

That is a very attractive place to hunt.

The portfolio makes the point clearly (sharing four of the portfolio companies out of 20).

EKAB is the market leader in preventive maintenance of high-voltage substations in the greater Stockholm area.

ILEMA is the market leader in Sweden within air emission measurements.

Kjellbergs is the Nordic market leader in actuators for vehicle-mounted tail lifts.

Intermercato is a specialized manufacturer of load attachments for heavy vehicles and machinery, and a world leader within its weighing system.

All these may not sound glamorous… but that is the point.

The best lower-middle-market businesses are often hiding in places that do not sound exciting at all: funeral products, hydropower turbines, air measurement, stainless equipment, technical textiles, sawmill aftermarket services.

That is often exactly where economics gets interesting.

I appreciated the tone management took in discussing 2025.

Henrik Mella did not present the group as if every business was firing at all times.

He highlighted stronger performers, but he was also candid about weaker areas.

It sounds like management is actually thinking like owners.

The bigger reason I find IDUN compelling is that the model is much harder to replicate than it looks.

Anyone can say they want to buy niche leaders.

Actually doing it is another matter…

You need to understand tiny industrial and service markets that almost nobody studies.

You need to know whether a company’s apparent leadership is real and durable.

You need to know whether management can continue running the business with autonomy.

And you need to build credibility with founders who care what happens after the sale.

Capital alone does not solve that.

The real moat in models like IDUN is not just dealmaking ability.

It is trust plus pattern recognition.

- - - -

It is encouraging to see that every week more of you are clicking through and learning how to access proprietary deal flow through CapitalPad. (A sponsor of this newsletter).

Their team has built a platform focused on profitable, so-called “boring” businesses in the $2 million to $15 million EBITDA range.

They are firm believers that the lower middle market remains one of the most attractive asset classes available.

To date, they have completed 10 acquisitions and are currently pursuing two live deals, each with a projected IRR of 25% or more.

For accredited investors, there is an opportunity to invest alongside them.

That said, while the current live deals are underwritten to projected IRRs of 25% or higher, there are, of course, no guarantees in investing and this does not constitute investment advice.

You can review the opportunity yourself at CapitalPad.com. CapitalPad is also a sponsor of this newsletter, so this is not investment advice, and you should conduct your own due diligence.

Click here to sign-up (for accredited investors only).

- - - -

This week’s podcast is with U.S. based Lacey Wismer, the founder of Hunter Search Capital.

Lacey has been investing in ETA since 2010. She has backed 100+ entrepreneurs and completed over 65 acquisitions. Family office patience with A-player urgency.

Search funds. Holdcos. Serial acquisition. Fundless sponsors...

These used to be separate lanes. Now they're merging into one asset class -- and it's growing exponentially.

We also covered two of the businesses her family has exited; one was a 35x MOIC outcome, and the other was a 100x MOIC outcome.

Here are the links to Spotify, Apple Podcasts, and YouTube.

That’s all for today.

This coming weekend I’m heading to NYC, the mecca of finance, as they say, so next week’s newsletter will be me sharing my lessons and takeaways from the meetings I’m going to have there.

Talk to you very soon.

Best,

Mike Markus / PrivateEquityGuy