- PrivateEquityGuy

- Posts

- from $20m to $200m in 16 month while the founder was "done"

from $20m to $200m in 16 month while the founder was "done"

A special edition for those looking for great deals

PrivateEquityGuy

September 04, 2025

You're 26; people give you $5 million, and you lose it all.

You then learn Buffett and Graham and turn $50 million into $5 billion while making $100 million yourself.

I think you just have to keep going in life!

Learning Buffett and Graham definitely helped. But even more importantly what Rainwater learned (according to the prior research done by a guy I talked to) was to give the money to people who were the best in the world at their investment area, and then watch the money multiply (Do you do that too?).

Richard Rainwater being one of the best capital allocators of his era (Bass family fortune going from ~$50M (1970) to ~$5B (by 1986) during Rainwater’s 16-year run)

I put together a tight breakdown of the Bass/Rainwater “$5B playbook,” with concrete deal sizes and outcomes.

The big dollar moves (with amounts)

Year | Company | What they did | Dollars in / stake | Outcome / proceeds |

|---|---|---|---|---|

1981–82 | Marathon Oil | Bought into takeover turmoil (Mobil tried to acquire Marathon; U.S. Steel ultimately bought Marathon). Classic event-driven trade. | Roughly $160M invested (implied; they made $160M profit, “doubling their investment”). | +$160M profit. |

1983–84 | Arvida Corp. (Florida real estate) | LBO of Arvida out of Penn Central with minimal equity; then flipped it to Disney for stock to put DIS shares in “friendly” hands. | $203.7M purchase; ~$20M equity (rest bank debt). Six months later Disney paid $214M in DIS stock; effective entry price to DIS for the Basses was about $7.50/share when DIS traded near $60 (because of how the swap was structured). | Turned ~$20M cash into ~$200M of Disney stock and a board foothold; set up the larger Disney trade. |

1984 | Texaco | Accumulated 25.6M shares (~9.8%); Texaco then “greenmailed” the Basses. | Cost disclosed in SEC filings: $891.2M spent; Texaco bought the stake back at $50/share (half in cash, half in preferred). | $1.7B received; +$390.7M profit crystallized. |

1984–86 (and beyond) | Walt Disney Co. | Built a massive position and helped install Eisner/Wells—classic “iconic but underperforming” blue-chip turnaround. | Initial 1984 check reported as $360M (UPI) to $478M (Fortune/Wikipedia). Stake rose to ~25% by late 1984 (after Arvida swap and open-market buying). | By 1986: ~$850M paper profit on the stake. By 1992: that 1984 investment was valued around $3.75B. |

The pattern to copy (if you’re distilling lessons)

Concentrate on a few big, asymmetric bets.

Use catalysts (leadership change, asset sales, takeovers) to accelerate value realization.

Exploit structure & financing (e.g., Arvida’s low-equity LBO → Disney stock).

Be pragmatic on exits (negotiate when it pays—Texaco).

To sum up:

Tactically, Rainwater ran concentrated positions, backed operators he trusted, and wasn’t shy about activism/negotiation to accelerate change. That combo - big brand turnarounds (Disney), energy event trades (Texaco/Marathon), and asset-backed real estate (Arvida) - is what powered the leap to ~$5B.

- - - -

If you’d like to invest in the next Rainmaker who makes big money moves with your capital: you should go and check out CapitalPad (a brand new sponsor of this newsletter).

You can own real, durable businesses that compound — all without running them day-to-day.

CapitalPad gives accredited investors access to curated SMB acquisitions—the kind led by searchers and independent sponsors buying established, profitable companies in sectors like home services, healthcare services, light manufacturing, IT and more.

You see a full deal room—financials, tax returns, sponsor profiles, the value-creation plan—and you co-invest on a per-deal basis with minimums starting at $25K. There are no management fees; CapitalPad only participates if investors get their capital back and profits are earned.

Learn more and apply at CapitalPad.com

- - - -

While doing my morning reading yesterday, I read timeless lessons from a gentleman who has made many acquisitions and done them well.

I think you might like these too:

Do great work, every time

One good deal usually leads to more

Outwork people and make clients happy

That’s how you grow fast

- - - -

As you know I like to read and study a lot…

I personally consider folks in the B2B SaaS space to be among the most competent.

Why?

Simply look at the multiples (see below P/E ratio 115!!) of the companies in that space.

That said, it would be dumb not to learn from them (something I do daily).

Here are takeaways on HARD WORK, LEVERAGE, and BEING SCARED from a gentleman who bootstrapped a B2B SaaS to $30–35M.

(probably receiving 9-figure offers to be acquired on a weekly basis)

1. All your results will come from your team, the people you hire and the DECISIONS/goals you decide to pursue.

2. Most entrepreneurs choose to OVERCOME staying in their comfort zone with little risk by working REALLY hard.

3. The biggest results come from LEVERAGE. Not work.

4. The biggest leverage comes from seizing opportunities and control of certain areas of the market before the others recognize their potential. To do this you have to take bets/risks on "theoretical" plays that might be wrong.

5. If you do not have some big bet that scares you and is not sure to work out....You are not going to get max leverage.

6. You have to see a potential future that isn't here yet or a sector of the market people are not seeing....and bet on it without the assurance of success.

- - - -

Met a founder of a $1.5m EBITDA company who was “done.”

He had two buyers: one was offering more $$$; the other showed a specific plan where they offered flexible hours, respected legacy, and a clean handover for the team.

The deal cleared not on price...

Culture, culture, culture.

- - - -

Heard a story about a woman who used to work for the FBI.

Then she was hired as an operator for a private equity backed traditional business.

She grew the company from $15m to $190m (through M&A).

Today she is in her 40s and is just getting started.

-

She’s coming to the podcast.

The people at ETA and independent sponsor space are super generous helping out to make this episode happen.

-

What has definitely helped with those warm intros is the weekly newsletter I write.

If you feel you’d like to have one but you know you don’t have enough time to write these, yet you’d STILL like to experience the upside (read: build relationships and trust at scale).

Reach out to David and Brandon at Spacebar Studios.

They’re offering three people or businesses a 2-week FREE trial.

They’ll set up your newsletter, send your first few editions, and prove the channel works—again, all that for free, so there’s really nothing to lose.

Start your free trial today at SpacebarStuidos.co

- - - -

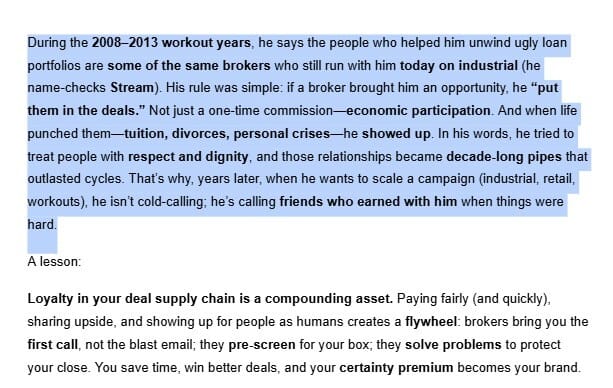

Btw, do you take care of the brokers you work with?

Take it from a man in his 40s who has done 100+ deals and built a ten-figure holdco.

Today he runs an investment firm and holding company with a dozen independently managed subsidiaries spanning financial services, healthcare, and real estate.

- - - -

You are not special... but even more importantly, THEY are not special either.

When reading and learning about people ("they") who have built very large investment firms, bought a lot of companies, done 50+ deals... they, too, have had moments when they had little cash, clean hands, and zero baggage.

Despite that, they kept going... or, better yet, their their wives/partners told them to keep going as they saw in them something MUCH more than themselves at those very moments.

Two lessons

1. Understand that "they" are all normal people.

2. Listen to your wife.

- - - -

How has been the week in the small holding company world?

Consumer loan company

We financed purchases worth approximately 1.4 million euros, and an additional 400,000 euros in credit were provided.

Buy-Now-Pay-Later purchases

- - - -

This week’s podcast:

Fundraising is one of the hardest things for any private equity partner...

Schwarzman from Blackstone on what Pete Peterson said to him after one of the failed meetings:

For Darrell from IMBIBA, the experience was no different:

“It was absolutely horrendous… we got to about $40m quite quickly and just could not raise the last $10m.”

“I hadn’t earned any income in 19–20 months… I was borrowing money from friends to pay mortgages.”

Today’s guests end up raising $50m.

Survived COVID and kept building.(show me better operators!!)

Today manage 12+ portfolio companies and already raising Fund III

Recent exit: 3× MOIC in <2 years

Full episode with Lizzie & Darrel from IMBIBA—how to survive shocks and still compound.

Enjoy.

Here are the links to Spotify, Apple Podcasts and YouTube.

That’s all for today.

Thanks a lot for reading and I’ll share a few updates again next week.

Take care,

PrivateEquityGuy / Mikk Markus